Income drawdown hub

This project aimed to reduce administration costs for pension providers and simplify the income drawdown process for their customers.

Project role: UX Designer & Digital Product Manager

Project length: 2 years

Project overview

Income drawdown has become the most popular option at retirement for Defined Contribution pension customers. However, due to relatively low volumes in the mass market and generally small pot sizes, the industry has been slow to invest in this critical part of the direct-to-consumer (D2C) retirement process. As a result, many customers opt to withdraw their entire pension as a lump sum.

This comes as no surprise, since providers currently generate limited income from auto-enrolment drawdown and have not built the D2C infrastructure needed to automate processes and manage more complex cases. Consequently, the system remains highly admin-intensive, costly to operate, and unfriendly to users. Most drawdown options are not readily available, and the reliance on paper-based applications makes accessing retirement funds a cumbersome and frustrating experience.

Initial findings

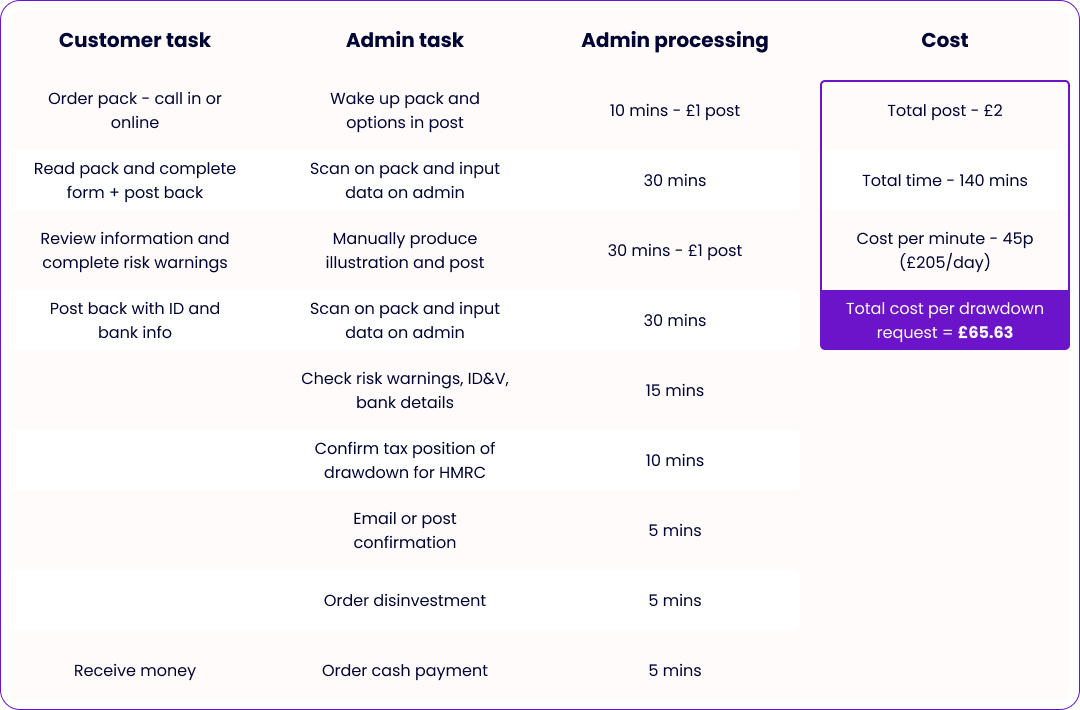

This project originated after multiple discussions with pension providers, who shared concerns about the inefficiencies in their drawdown process. Many described it as overly time-consuming and expensive to administer. Most providers relied on paper-based applications, requiring documents to be posted back and forth between the provider and the member. As a result, the withdrawal process could take several weeks—or even months—to complete. These insights were supported by a thorough review of the existing procedures.

Process mapping

This project originated after multiple discussions with pension providers, who raised concerns about the inefficiencies of their drawdown process. Many described it as overly time-consuming and costly to administer. Most relied on paper-based applications, requiring documents to be sent back and forth between the provider and the member. As a result, the withdrawal process often took weeks—or even months—to complete. These findings were further validated through a thorough review of existing procedures.

Once the stages of the new digital process were defined—including adjustments for updated FCA regulations—we worked closely with several pension providers to map out the content required at each stage through collaborative workshops. This hands-on approach ensured the solution was both fully compliant and market-leading.

Collaborative workshops

Once we had clarity on the stages required for the new digital process—including updates in FCA regulations—we collaborated closely with several pension providers to map out the necessary content at each stage through a series of workshops. This close partnership enabled us to ensure the content was accurate, fully compliant, and aligned with market-leading standards.

With the drawdown withdrawal journey clearly defined, we then turned our attention to the end user: the customer.

Our focus was to design a solution that makes it easier and faster for individuals to access their pension funds—removing long-standing barriers such as:

An overcomplicated, paper-heavy process

Pension industry jargon that confuses customers

Lengthy delays in receiving funds after making a withdrawal request

By directly addressing these pain points, we’ve developed a streamlined, user-friendly product that puts customers in control of their retirement income.

Initial design

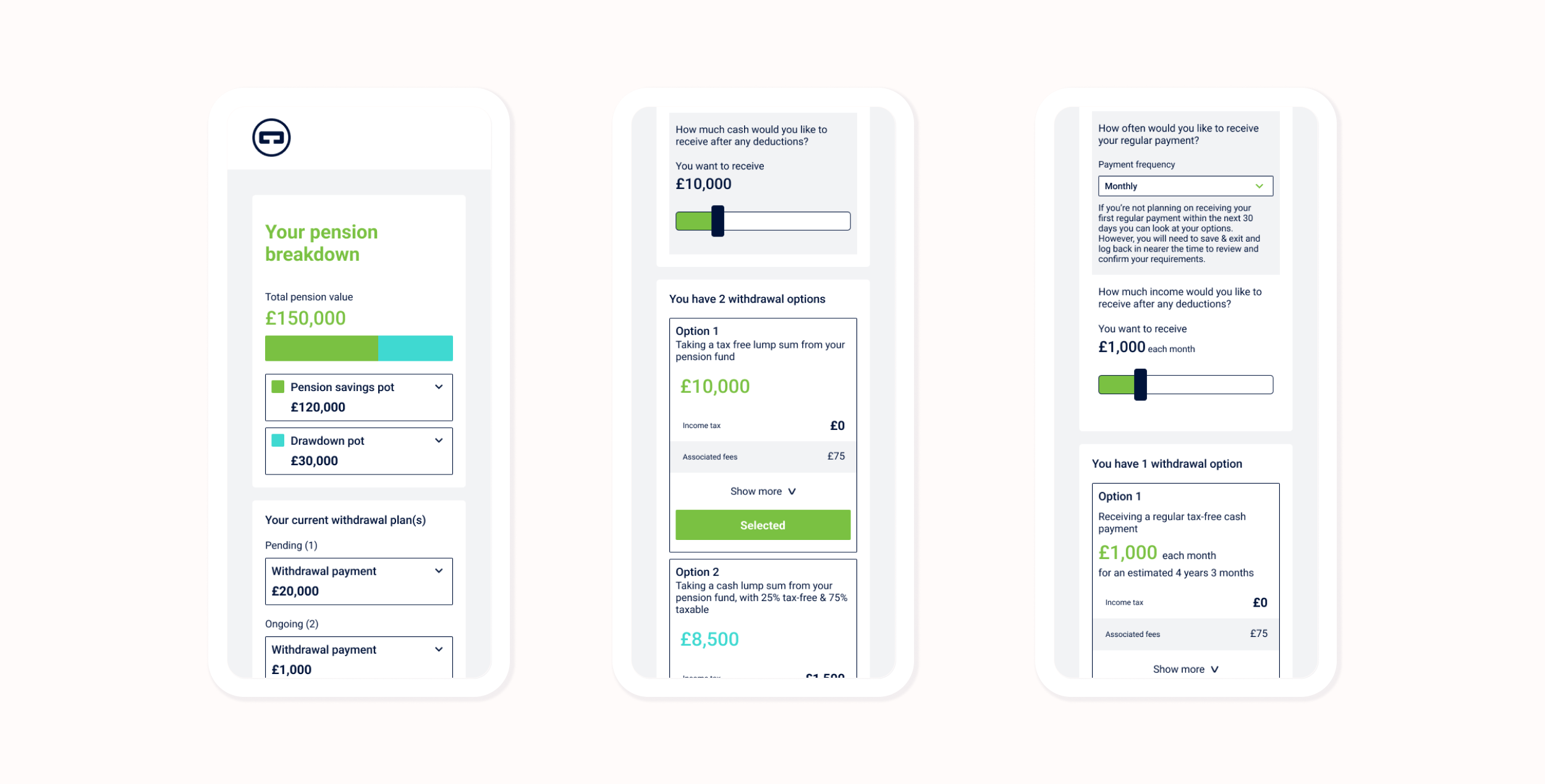

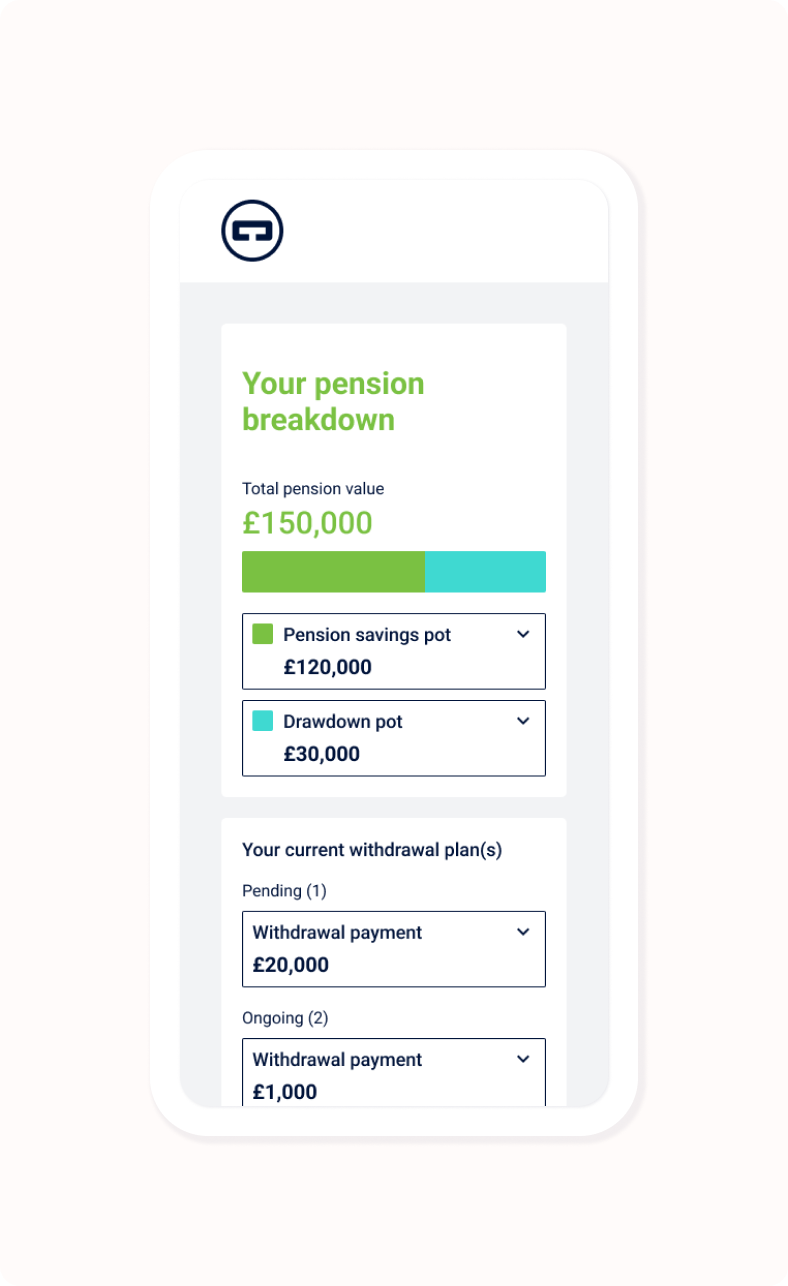

With the drawdown withdrawal process stages defined, we were then able to shift our focus to the end user—the customer—ensuring the product was intuitive and accessible, even for those with little or no prior pension knowledge. This required extensive work, including the creation of clear wireframes, screen prototypes, and carefully crafted user journey wording to ensure the final product met both pension provider requirements and customer expectations.

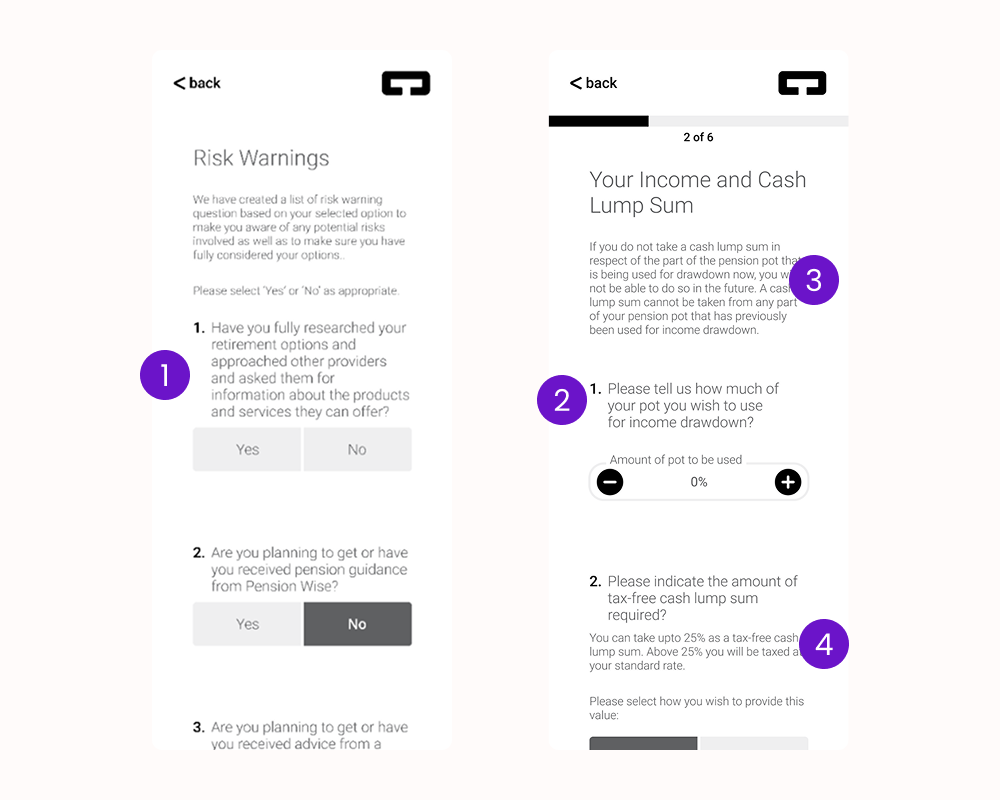

Initial user testing highlighted several key recommendations:

Present one risk warning question per page to avoid overwhelming users.

Simplify and streamline the wording throughout the journey.

Clearly explain the customer’s fund split to improve financial understanding.

Rework how different withdrawal types are presented, making the options easier to navigate.

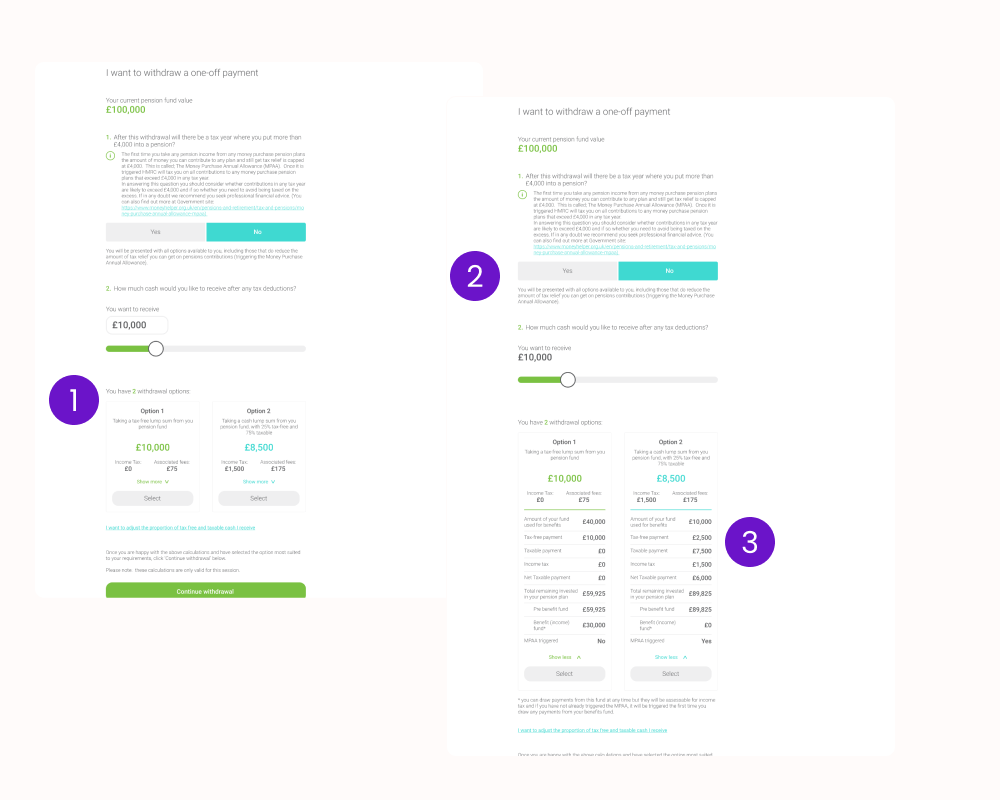

Withdrawal Screen Enhancements & Recommendations

As the Withdrawal screen required more development than other parts of the workflow, it became the central focus of the project. The goal was to improve usability—especially for users with limited pension knowledge—by creating a more intuitive and supportive experience.

Key improvements included:

Simplified Language: Options were presented in clear, accessible terms, avoiding technical jargon like "withdraw" in favor of language that reflects what users want to achieve.

User-Centered Framing: Questions were rephrased to focus on user goals, helping them better understand their choices.

Progressive Disclosure: Only the most relevant content and questions were shown initially, with the option to reveal more detailed information as needed. This kept the interface clean and reduced cognitive load.

Side-by-Side Comparisons: Users could view and compare all relevant withdrawal options in one place, supporting informed decision-making.

Expandable Sections: Complex information was tucked behind expandable elements, preventing users from feeling overwhelmed while still making details accessible.

These enhancements aimed to reduce barriers to engagement, support confident decision-making, and create a more user-friendly pension drawdown experience.

Project outcome

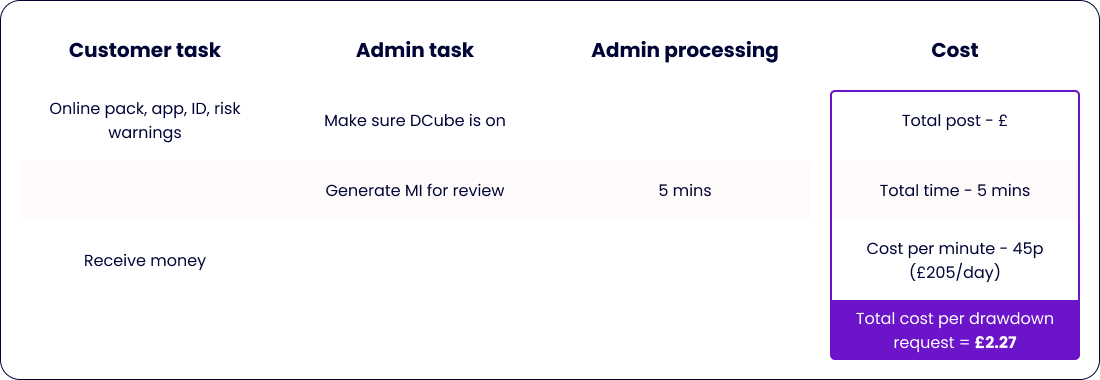

DCube simplifies and lowers the cost of the drawdown setup process, making it more accessible to the wider public—beyond those who can afford traditional financial advice. By eliminating manual processing and replacing multiple forms and applications with a streamlined digital journey, the platform significantly accelerates setup times.

CTC’s DCube product is currently used by a diverse range of pension providers and serves tens of thousands of users annually, with a withdrawal journey completion rate exceeding 95%.